A pipe burst is every homeowner’s nightmare. Whether it happens in the middle of the night or while you’re away from home, a burst pipe can dump gallons of water into your property in minutes — ruining floors, walls, cabinets, and personal belongings.

In Florida, where aging plumbing, shifting foundations, and extreme temperatures can all contribute to pipe failure, homeowners frequently deal with pipe bursts and the devastating water damage that follows.

So, what should you do if a pipe bursts in your home?

And how do you make sure your insurance actually pays what you need?

This guide breaks down:

- What to do immediately after a pipe bursts

- What homeowners insurance typically covers

- How to document the damage properly

- Why hiring a public adjuster can make all the difference in your claim

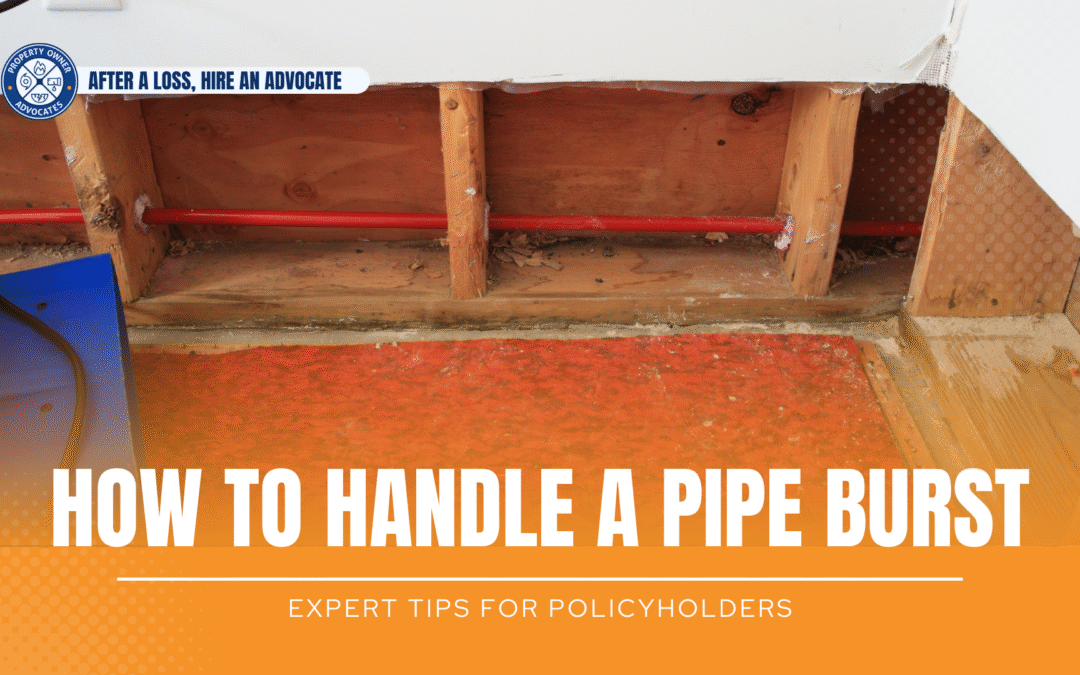

First Steps After a Pipe Burst

If a pipe has burst in your home, act quickly to minimize the damage:

- Shut off the main water valve to stop the flow of water.

- Turn off electricity in the affected area to avoid shock.

- Take photos and videos of all visible damage before cleaning up.

- Contact a licensed public adjuster before filing a claim — they will help preserve evidence and also be able to guide you through the damage mitigation and claim filing process.

Download our FREE Water Claim Guide

The earlier you start documenting damage, the stronger your claim will be.

Does Homeowners Insurance Cover Burst Pipes?

Yes — most Florida homeowners insurance policies cover sudden and accidental water damage from pipe bursts. That typically includes:

- Water damage to flooring, drywall, ceilings, and cabinetry

- Mold remediation (if mold is a result of the covered peril, mold itself is NOT a covered loss)

- Temporary repairs and mitigation

- Tear-out costs to access the broken pipe

- Additional living expenses (if your home is deemed “unlivable”)

Wondering how Additional Living Expenses coverage works? Read more here

However, insurers may deny or undervalue your claim if they believe the pipe burst was caused by:

- Corrosion or old plumbing

- Long-term neglect or lack of maintenance

- Previous unrepaired leaks

- Foundation movement or poor installation

It is also worth pointing out that pipes themselves are often not covered – just the labor and resulting damage caused by gaining access to the pipes in addition to any other damages caused by a covered peril.

Navigating these technicalities and policy language is where an experienced public adjuster will be able to help.

Common Pipe Burst Scenarios in Florida

Coverage Checklist

- Slab leak: A pipe breaks beneath your concrete foundation, causing water to rise through tile or flooring (not usually covered)

- Wall or ceiling burst: Water pours through drywall from a ruptured pipe in the ceiling or wall cavity. (usually covered)

- Outdoor pipe failure: Bursts in irrigation or pool lines flood exterior walls or nearby rooms. (not usually covered)

- Washer, water heater, or refrigerator line: Supply line bursts and floods kitchen or laundry area. (usually covered)

Each situation is different — and not all insurance adjusters will interpret your policy the same way. That’s why expert representation matters.

What Kind of Water Damage That Is (Usually) Covered vs. What’s (Usually) Not Covered:

Covered:

- Drywall, insulation, and flooring removal and replacement

- Mold remediation

- Water-damaged construction materials and finishes

- Water damage to personal property

- Hotel stays or temporary housing

Not Covered:

- The cost to repair the actual pipe (most policies exclude this)

- Long-term or pre-existing damage

- Poor maintenance or DIY plumbing errors

We’ll review your specific policy to determine what’s covered — and push back if your insurance company tries to deny a rightful claim.

How to Document Your Pipe Burst for a Claim

Insurers require solid documentation to process your claim.

Be sure to gather:

- Photos/videos of the damage and broken pipe

- A plumber’s report detailing the cause and location of the burst

- Receipts for emergency repairs or water mitigation

- Moisture readings and/or mitigation invoices and mold test results

- Your written timeline of what happened and when

Important: Don’t throw away damaged items or demo materials until a public adjuster or your insurer has seen them.

Why Work with a Public Adjuster?

You have every right to file and negotiate your claim on your own (and in certain cases it may actually make sense to), just know that Insurance companies aren’t handling your claim on their own.

Insurance companies have a team of professionals that help them defend claims, this can mean defending their denial of coverage, their estimated claim value, or even their bad faith practices. This is one of the reasons many homeowners find their initial payout is far less than what it actually costs to restore their property.

A licensed public adjuster at Property Owner Advocates will:

- Inspect and assess the true scope of damage

- Use thermal and moisture imaging to detect hidden issues

- Prepare a professional estimate that reflects real costs

- Negotiate directly with the insurer

- Reopen a denied or underpaid claim

Get Help After a Pipe Burst — Before It’s Too Late

Water damage spreads fast, and so do insurance headaches. If your Florida home suffered a pipe burst, don’t go it alone.

Call Property Owner Advocates for a free consultation. We’ll inspect the damage, review your policy, and help you fight for a proper settlement.

Call Now or Schedule an Appointment Online

Don’t wait for mold, stress, or red tape to pile up. Let us advocate for you.